|

Company Name |

Zander Insurance Group |

|

Founded |

1927 (Nearly a Century of Service) |

|

Headquarters |

Nashville, Tennessee |

|

CEO |

Jeffrey J. Zander (Fourth Generation Family Business) |

|

Main Services |

Term Life, Auto, Home, Disability, Identity Theft Protection, Business Insurance |

|

BBB Rating |

A+ (Accredited since 2004) |

|

Phone Number |

(800) 356-4282 |

|

ICON POLLS Rating |

2.9 out of 5 stars |

Overview

You've probably heard about Zander Insurance if you listen to Dave Ramsey or follow personal finance advice online. The company has become a recognizable name in the insurance world, and for good reason. With nearly 100 years of history, Zander has managed to stay relevant and competitive in an industry that's constantly evolving. But here's what we wanted to know: Does the reputation match the reality? After spending weeks researching customer reviews, testing their platforms, and analyzing their offerings, we found a company that's genuinely trying to do right by its customers, but with some real frustrations that hold it back. Our 2.9 out of 5 star rating reflects this complicated reality. Zander excels in certain areas, particularly in life insurance accessibility and pricing competitiveness, but several customer service challenges emerged that affect overall satisfaction ratings and keep this from being a clear winner.

Broker Services and Coverage Options

Here's something important to understand about Zander that many people don't realize initially: they're not an insurance company themselves. Instead, they function as an independent broker, which is actually really good news for you. Think of it like comparing insurance prices across multiple providers, but instead of you doing all the legwork, Zander's team does it for you. They've built relationships with major A-rated and A+ rated insurance carriers including Protective, Banner Life, Mutual of Omaha, Prudential, and Lincoln Financial. When you get a quote from Zander, they shop your needs across 15 to 20 different companies depending on what you're looking for. This means you're not locked into one carrier's pricing or underwriting standards. You get genuine competition working in your favor.

The breadth of services Zander offers is impressive. Yes, they're famous for term life insurance, but they also handle auto insurance, homeowners insurance, health insurance, disability coverage, commercial business insurance, and identity theft protection. If you're looking to consolidate your insurance needs with one company, Zander can genuinely help with that. You could theoretically manage your entire household insurance portfolio through them. However, there's one deliberate limitation you should know about: Zander exclusively sells term life insurance. You won't find whole life, indexed universal life, or any of those cash value products that traditional insurance agents push. This isn't a shortcoming or an oversight. It's an intentional business decision rooted in the company's philosophy. Zander's leadership, aligned with Dave Ramsey's financial teachings, genuinely believes that term insurance provides better value for most families. Their argument is straightforward: pay less, get solid protection, and invest the difference yourself. Whether that appeals to you depends on your own financial philosophy.

What we appreciated during our research was the transparency about this approach. Zander doesn't hide the fact that they only sell term. They explain their reasoning openly. That's refreshing in an industry where some companies obscure their limitations or try to push customers toward products that benefit the agent more than the customer.

Customer Service Experience

Here's where Zander gets really interesting, because we found something unusual: glowing individual reviews paired with frustrating systemic complaints. When customers talk about the actual agents they worked with at Zander, they're remarkably positive. One customer described their agent as having 'excellent customer service and attention to detail, great rates, and they deal with only A plus companies for insurance.' Another customer raved about how patient and personable their agent was, walking them through the application process with genuine kindness and efficiency. We found multiple examples of customers praising Zander's responsiveness, professionalism, and willingness to answer questions. Many people specifically mentioned that agents went above and beyond, even staying available after hours to help. These aren't outlier reviews either. Many customers genuinely appreciate working with Zander's team.

But here's the problem that keeps appearing over and over in reviews, and it's significant enough to impact our overall rating: Zander's follow-up communication strategy is aggressive to the point of harassment for many customers. After you submit your contact information or begin an application, the phone calls start. One customer reported getting calls almost daily for months after declining coverage. Another described it as a 'harassment campaign,' noting that they tried blocking numbers, but Zander just called from new numbers. The pattern gets even worse when customers explicitly ask to be taken off the list. Some people have reported requesting removal multiple times and continuing to receive calls and texts weeks or months later. We found complaints where customers got mailed letters in addition to phone and text contact. The Better Business Bureau has logged multiple complaints about this exact issue. To their credit, Zander has acknowledged these problems and says they've made changes. They claim to have internal do-not-contact lists and have reinforced training with staff about respecting customer preferences. But the complaints continue to come in, which suggests the changes haven't fully solved the problem.

This creates a genuine dilemma. Individual Zander agents are often genuinely pleasant and helpful. But if you're someone who values your privacy and dislikes aggressive sales tactics, this follow-up approach will frustrate you. It's worth considering whether you're comfortable with that initial experience before reaching out to Zander. One customer summed it up well: 'I wanted to like them due to their Dave Ramsey connection, but I will never do business with them due to this harassment.'

Another important detail: once you have a policy with one of Zander's partner companies, customer service and claims handling go through that carrier, not through Zander. So if something goes wrong with your claim or you need support, you're dealing with the actual insurance company, not Zander's agents. This is actually pretty standard for brokers, but it's worth understanding upfront. You get Zander's help shopping for the policy, but the ongoing relationship is with the underwriting company.

Identity Theft Protection Services

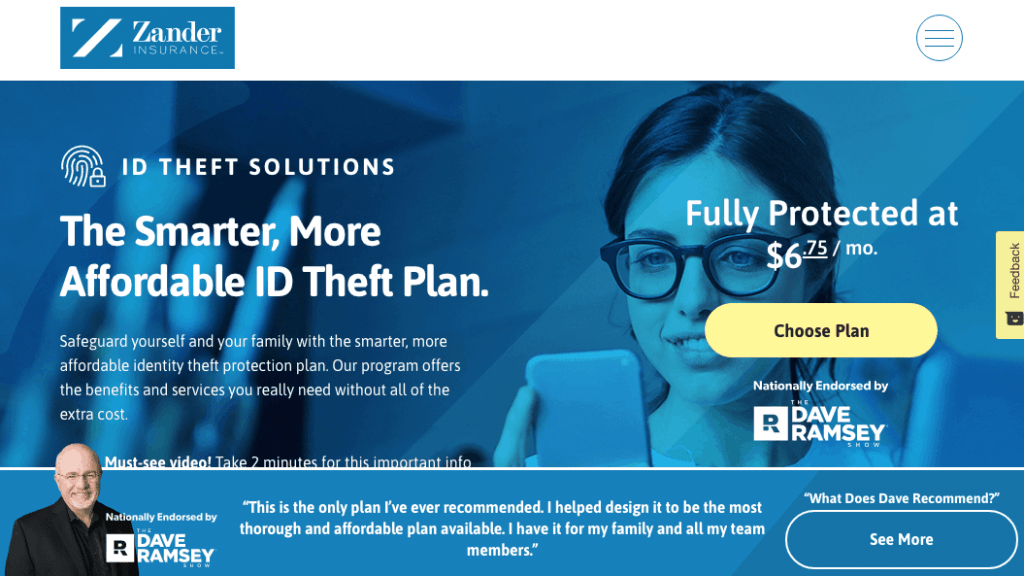

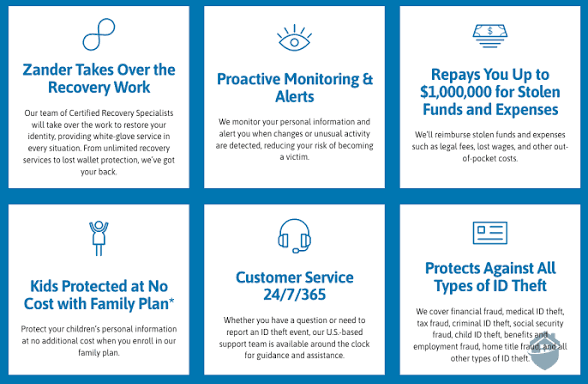

Let's talk about something Zander actually does really well and at prices that honestly surprised us. Their identity theft protection service is legitimately affordable. We're talking 6.75 dollars per month or 75 dollars per year for individual coverage. For a family plan, it's 12.90 dollars monthly or 145 dollars annually. Those prices are genuinely competitive, often cheaper than what you'll find elsewhere. When you consider what you actually get for that price, it becomes even more impressive. You get monitoring across multiple threat areas including credit reports, personal information databases, dark web scanning, Social Security number monitoring, change of address alerts, and data breach notifications. The company also includes a child information scan feature, which is particularly valuable if you have kids. That tells you immediately if any of your children's information has been compromised.

Now, we should be honest about what's NOT included. Zander doesn't offer traditional credit monitoring or credit score tracking like some of their competitors do. You won't see daily credit score updates or credit report snapshots. This is a real limitation if you rely on that feature. However, Zander does provide a credit lock feature through Experian, which will alert you when someone tries to access your credit or applies for new accounts in your name. So you get the security benefit, just not the credit tracking piece.

What truly stands out is Zander's recovery team. If your identity actually gets stolen, Zander connects you with a team of Certified Recovery Specialists who are available 24/7. These aren't automated systems or customer service reps following scripts. These are trained specialists dedicated to helping you fix the mess. They'll work with you to create a recovery plan, contact financial institutions, dispute fraudulent charges, and handle all the recovery logistics. There are no time limits and no monetary caps on their assistance, which is unusual and genuinely valuable. Zander will reimburse you up to 1 million dollars for stolen funds and expenses from identity theft, and family plans cover up to 2 million. That includes legal costs, which matters if you need to pursue legal action to clear your name.

If you want additional protection, Zander offers an Elite tier that adds a password manager, VPN service, and antivirus software to the Essential package. It's a nice option if you want comprehensive digital protection alongside identity theft monitoring.

You manage everything through a web-based portal and mobile apps for iOS and Android. The account setup is refreshingly straightforward. You provide basic personal information and payment details, and two-factor authentication is automatically enabled. No hunting through security settings to find it. One detail customers appreciated: you can allow the system to remember your device for 60 days, reducing the need to authenticate repeatedly. Alternatively, you can maintain 2FA for every single login if you prefer maximum security.

Login and User Experience

The user experience at Zander varies significantly depending on which product you're using, which we found to be one of their frustrating inconsistencies. For auto and home insurance customers, everything goes through a mobile app and web portal. The good news is that it's available 24/7, so you can access your information whenever you need it. You can download your insurance ID cards instantly, which is genuinely convenient, especially when you're at a car rental desk and the agent needs proof of coverage. You can also request policy changes, report claims from the desktop version (though not on mobile, which is odd), contact representatives, and review detailed coverage information.

Here's where the experience gets frustrating. Reviews of the mobile app are decidedly mixed, and honestly, they lean negative. Users report frozen screens, unresponsive buttons, error messages, and functionality problems, particularly on current iOS versions. One customer said, 'On my iPhone with current iOS and current version of this app, it simply does not work. Try to view cards, screen freeze. Virtually everything I try to open results in unresponsive buttons and frozen screen with error messages. Ridiculous. As a new customer with Zander, I'm not impressed.' Multiple users echoed similar frustrations. What's particularly frustrating is that for auto and home insurance, the mobile app is basically the only way to manage your account. There's no functional web alternative that works well. If the app isn't working, you're stuck.

We also found complaints about password reset functionality. Some users encountered error messages saying their password 'must not be empty' even though it clearly wasn't. These technical issues suggest that Zander's tech team hasn't fully stress-tested the user interface in real-world conditions. It's the kind of problem that frustrates users and creates a bad first impression.

For identity theft protection, the experience is notably better. You get a separate web-based member portal and dedicated mobile apps for iOS and Android. The signup is straightforward and takes just a few minutes. The dashboard itself is clean and readable, displaying alerts and important information clearly. Two-factor authentication is enabled by default, which we appreciated for security reasons. The portal functions smoothly in browser testing, and the information architecture makes sense. Mobile app functionality is more limited than the web version, but users reported that the core functions work as expected.

Overall, the user experience inconsistency between products bothers us. Zander seems to have invested in the identity theft protection experience but let the auto and home insurance platform struggle. If you're considering Zander primarily for auto or home insurance, you should know that accessing your account through their app might be frustrating. If you're going for identity theft protection specifically, the experience is considerably smoother.

Frequently Asked Questions

1. Is Zander Insurance a legitimate company or a scam?

This is the first question most people ask, and the answer is straightforward: Zander is absolutely legitimate. The company was founded in 1927, which means it's been around for nearly a century. That's not a short time period. It's now managed by the fourth generation of the Zander family, which tells you something about stability and commitment to the business. They maintain an A+ rating from the Better Business Bureau and have been BBB accredited since 2004. That A+ rating is the highest possible, which matters. Zander's partnership with Dave Ramsey, a nationally recognized personal finance educator and author, provides additional validation. It's worth noting that Dave Ramsey doesn't endorse every company that asks. He has a reputation to protect. The company works exclusively with A-rated and A+ rated insurance carriers that are well-regulated and financially sound. Moody's and other rating agencies scrutinize these carriers carefully. So while Zander has faced customer complaints regarding sales practices and follow-up communication, these operational issues don't reflect on the company's legitimacy. You're dealing with a real company that's been in business longer than most of us have been alive. That said, being legitimate doesn't mean it's perfect, which is why we encourage you to read our full review.

2. Why does Zander only offer term life insurance, not whole life?

This is a deliberate business philosophy, not a limitation or oversight. Zander's leadership believes, and Dave Ramsey has taught this for decades, that term life insurance represents superior value for most people. Here's the basic logic: term life insurance is straightforward. You pay a monthly premium, you get death benefit protection for a specific period of time, and that's it. If you die during the term, your beneficiaries get the death benefit. If you don't, the policy expires. The monthly cost is typically quite low, especially for younger people. Whole life insurance and indexed universal life, by contrast, have much higher premiums and include a cash value component that grows over time. The agent commissions on whole life are also significantly higher, which is worth considering when an agent is pushing it. Zander's position is that customers come out ahead by buying affordable term coverage and investing the premium difference themselves. Over 20 or 30 years, that approach typically results in more accumulated wealth than paying higher premiums for permanent coverage. Whether you agree with this philosophy depends on your own financial goals and beliefs, but at least Zander is transparent about their position rather than hiding it.

3. How much do Zander Insurance quotes cost, and do medical exams apply?

Pricing varies dramatically based on multiple factors. Your age, health status, occupation, tobacco use, the coverage amount you want, and the length of the policy term all affect the final price. A 32-year-old nonsmoker in excellent health will pay dramatically less than a 55-year-old with health conditions. That's why generic pricing doesn't mean much. The good news is that Zander offers instant online quotes, so you can get a personalized estimate without talking to anyone. You fill out a questionnaire, and you get an estimated quote immediately. Regarding medical exams, here's what actually happens: Zander partners with multiple carriers, and policies vary. Some carriers require traditional medical exams where a nurse visits your home or you visit a clinic. Others offer simplified underwriting where you answer health questions but don't take an exam. And some offer guaranteed issue policies with no exam and no health questions. The tradeoff is pretty logical: no medical exam means higher premiums because the insurance company can't verify your health. They're taking on more risk, so they charge more. But for people with health conditions or those who want quick approval, the no-exam options might be worth the higher cost. When you get quoted, the system will clearly indicate which policies require exams and which don't. This is one area where Zander's broker model actually helps you. You get to see multiple options instead of being locked into one carrier's underwriting requirements.

4. What is Zander Insurance's phone number, and how do I contact customer service?

The main customer service number is (800) 356-4282, available during business hours. If you're calling about identity theft protection specifically, there's a dedicated line at (888) 210-3274. Beyond phone support, Zander offers multiple contact channels. You can reach out via email at [email protected]. They have a live chat feature on their website that's available during business hours, which is convenient if you prefer written communication. The company maintains a comprehensive Help Center on their site with answers to common questions, which might solve your problem without needing to contact anyone. One thing to understand: response times vary. If you initiate contact with Zander, expect follow-up calls if you don't explicitly tell them to stop. We recommend being very clear about your communication preferences upfront to avoid the aggressive follow-up we mentioned earlier in the review.

5. How do I cancel my Zander Insurance policy or identity theft protection plan?

Cancellation processes differ depending on what you're canceling. For identity theft protection plans, the process is actually relatively straightforward. You can cancel anytime without penalties by contacting customer service. You can reach out through the website form, phone, email, or live chat. If you cancel within 14 days of subscribing, you get a full refund. Cancel after 14 days, and you lose the refund, but your service continues through the end of the term you already paid for. No surprise charges after cancellation. For auto, home, and other insurance policies, the cancellation process is different because Zander is the broker, not the underwriter. The actual insurance company handles cancellation. You'll contact your specific insurance carrier directly using the contact information on your policy documents. This is one thing that can be confusing for people, so we wanted to flag it clearly. Since you bought the insurance through Zander but the policy is with another company, that company manages cancellation. If you're unsure which company underwrites your policy, you can call Zander at the number above, and they'll help you figure out who to contact.

6. Does Zander Insurance require a medical exam for term life coverage?

The short answer is: sometimes, but not always. Remember that Zander partners with multiple insurance carriers, and each carrier has different underwriting requirements. Some absolutely require medical exams. Some offer simplified issue policies where you answer a health questionnaire but don't have a doctor involved. And some offer guaranteed issue policies with no exam and no health questions at all. The catch with the no-exam and guaranteed-issue policies is that the premiums are higher. Think about it from the insurance company's perspective: if they're not getting medical confirmation of your health, they're taking on more risk, so they charge accordingly. If you have a pre-existing health condition or you're concerned about getting approved, the no-exam options might be worth the premium increase. If you're young and healthy, you might save money by going with a carrier that requires an exam because you'll get better rates. Zander's job is to show you what's available so you can make an informed decision. When you request a quote, the system will clearly explain which policies require exams and which don't. You'll see the premium differences so you understand the tradeoff. This is actually one of the genuine advantages of working with a broker rather than a single carrier: you get options.

7. How does Zander Insurance work compared to buying directly from an insurance company?

This is a fundamental question about business models. Zander operates as an independent broker, meaning they don't underwrite or issue insurance policies themselves. Instead, they work as an intermediary between you and actual insurance companies. When you go to Zander, they evaluate your insurance needs, shop rates among multiple partner companies, and present you with options. Zander's agents help you understand the products and answer questions. You pick the option that makes sense for you, and Zander facilitates the application process. Direct insurance companies work differently. You go directly to State Farm, for example, or Geico, or Progressive. The company evaluates your needs and presents you with their products only. They're the insurance company, the agent, and the claims processor all rolled into one. So what's better? There are genuine tradeoffs. The broker model, which is what Zander uses, gives you access to multiple carriers without contacting each one separately. You get rate shopping and comparison built in. The disadvantage is that after purchase, you work with the insurance company for support and claims, not with Zander. So if something goes wrong, you're dealing with the carrier, not the broker. Direct carriers give you a consistent point of contact throughout the relationship. Everything goes through one company. The disadvantage is that you're only seeing that company's rates and products. You might get a better deal elsewhere, but you won't know about it unless you shop around yourself. For most people, Zander's broker model results in better pricing because of the rate shopping, but the relationship might feel less personal after purchase.

8. What security features does Zander Identity Theft Protection include, and how does the dashboard work?

Zander Identity Theft Protection uses a web-based portal where security is taken seriously. Two-factor authentication is enabled by default when you create your account, which we appreciated. You have flexibility with how strict you want the authentication to be. You can allow the system to remember your device for 60 days, so you're not authenticating every single time you log in. Or you can keep 2FA enabled for every login if you're more security-conscious. The dashboard itself is designed to be readable and user-friendly. When you log in, you see your monitoring alerts and key information displayed clearly. You're not hunting through menus to find important details. The monitoring itself covers multiple threat vectors: credit reports, dark web activity, Social Security number usage, new account creation, data breaches, and personal information databases. If you have children, the child information scan monitors whether any of your kids' information has been compromised, which is particularly valuable. Premium tier plans add password manager functionality, VPN service, and antivirus software, all sourced from reputable security providers. Mobile apps for iOS and Android provide on-the-go access to your account, though the mobile versions have fewer features than the full web portal. That's pretty typical for identity theft protection services. The recovery team sits behind all of this. If something does happen and your identity is compromised, you're not navigating recovery alone. You have trained Certified Recovery Specialists available 24/7/365 to help. The platform uses secure data encryption, and your information is protected according to current security standards. Overall, the security architecture seems solid, and we didn't find complaints about data breaches or security problems in our research.

Comments (0)